CoreWeave: A Masterclass in Financial Engineering

Dissecting the capital structure behind the fastest growing AI cloud provider.

Disclaimer

This is not financial advice. CoreWeave is a volatile stock. I wouldn’t recommend it for those who lack conviction.

Financials

Stock: CoreWeave ($CRWV)

Price: $83.3

Market Cap: $45.5B

1 Year Price Target: $115 (+38%)

Position: 5% of portfolio

Sector: AI Data Centers

Introduction

Back in early April, I put out an article called a macro note on AI. That article marked the bottom of the AI trade in 2026, and every name I listed re-rated aggressively over the next month. Directionally, my read was correct; however, I underestimated the true scope of the growth both Anthropic and OpenAI would see this year. Here’s what I said at the time.

“The above chart is from Anthropic directly and is already out of date. The correct run rate is closer to 25+ billion as of this article's publication. It is likely they exit the year at $60B+ ARR”

Anthropic has recently reached a $60B run rate, implying they should exit the year at $100B+. If we include OpenAI in the mix and make an estimate, I’d guess the aggregate of the two is at least $150B by year-end. In my view, the AI trade will continue to re-rate higher, and we are setting up for one of the best bull runs in the market’s history. CoreWeave, a leading cloud provider in this space, will benefit from both the tailwinds of the AI trade and from trading at a discount to its intrinsic value today.

The thesis on this one is quite simple. Despite a number of AI names being re-rated, CoreWeave has been left behind. The business, specifically its debt, is fundamentally misunderstood and is acting as an overhang on the stock price. CoreWeave has a $100 billion backlog. They’ll hit $20 billion in ARR this year and comfortably exit 2027 at $30+ billion in ARR. In addition, CoreWeave is the best cloud provider for deploying and running NVIDIA GPUs at scale. They outstrip big names such as Microsoft, Google, and Amazon and deliver higher-quality service than other well-known neoclouds like Nebius and Iren. All they need to do is continue to execute, and the market will begin to appreciate this story, leaving substantial upside for a re-rating.

CoreWeave’s origins

CoreWeave was founded in 2017. The founders, Michael Intrator, Brian Venturo, and Brannin McBee, were all commodity traders who ran a GPU on the side for fun, mining Ethereum. What started as a fun hobby started to deliver real profitability. They’re able to take the Ethereum they mined, sell it, and invest it into more GPUs, which allows them to mine even more Ethereum and grow the business. While this worked well at first, they quickly ran into a problem. This business was reliant on a very volatile crypto market. Ethereum’s price would peak at $1,200 per ETH before crashing back down to $90 in December 2018.

The business's economics were much better when ETH was at $1,200 rather than $90. This meant that the business swung from wild profitability to significant loss. The founders realized that mining Ethereum long-term was not a sustainable business, and that’s when they came up with a clever alternative. CoreWeave would deploy GPUs and sell raw compute to customers on contracts for things such as rendering graphics or early machine learning workloads. When the GPUs were idle, they’d then use them to mine Ethereum. This meant that, no matter what, they were always generating revenue. During crypto winters, they were able to break even or turn a profit, while their competitors went under. Then, they’d acquire their competitors’ GPUs at fire-sale prices, allowing them to sign more contracts or mine more Ethereum.

They would rinse and repeat this business model through cycles and continue to scale the business this way until 2022. Around this time, they saw machine learning workloads starting to take off and become one of their most popular business lines. NVIDIA released its most recent GPU, Hopper (H100S), in 2022. Coincidentally, Ethereum was changing the way its underlying blockchain worked, which meant mining Ethereum was no longer a viable business model. CoreWeave took a gamble and acquired $100m worth of Hopper GPUs, believing AI was on the precipice of takeoff, and that demand would surge.

This gamble would soon pay off; later that year, ChatGPT would be released, thereby beginning the AI revolution. Given that CoreWeave had already been deploying, running, and selling these contracts, they were well-positioned to pounce on the massive increase in demand. Those H100S they had bought speculatively earlier were among the few GPUs available and were quickly contracted and sold. The founders realized AI was the future of their business. The years spent building and operating GPU clusters for crypto gave CoreWeave something that would become incredibly valuable: operational expertise. They knew how to deploy AI clouds before the rest of the market did.

CoreWeave Today

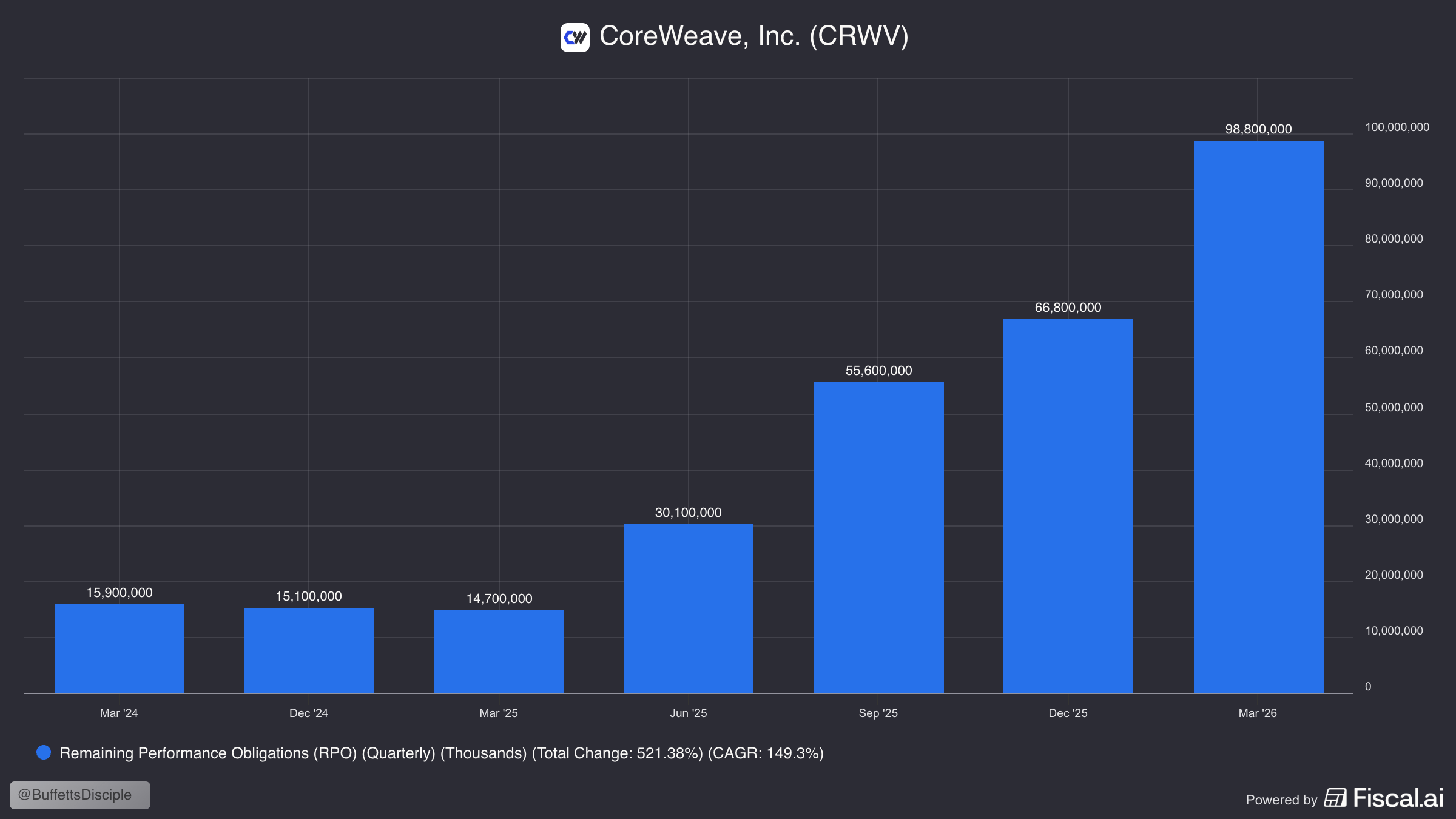

CoreWeave's value proposition is simple: it provides the highest-quality NVIDIA GPU cloud at competitive prices. Running tens of thousands of GPUs is not as simple as just buying and running the hardware. It requires networking, power, cooling, scheduling software, monitoring, and constant maintenance to maintain high utilization. Customers are committing billions of dollars to multi-year contracts; they’re not going to risk large sums and be stuck with a mediocre cloud. CoreWeave’s exceptionalism has shown up in their backlog, up 3x Year over year. Today RPO stands at $100B.

If CoreWeave wanted to, it could aggressively expand this backlog. However, they’re intentionally selective about whom they partner with when diversifying their business for the long term. They’re also prioritizing higher-quality partners (such as Jane Street) that provide recurring business and are in strong financial shape.

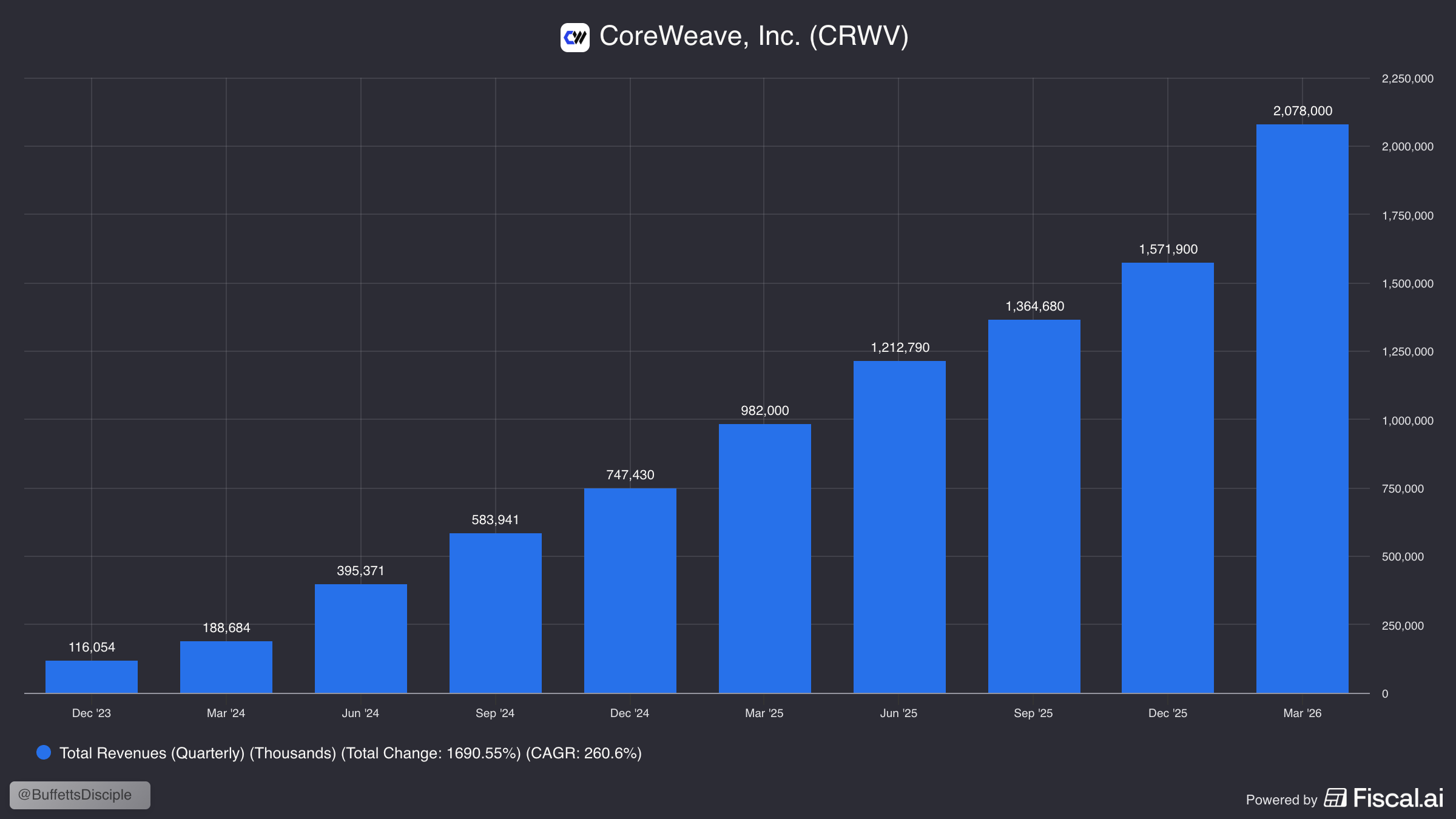

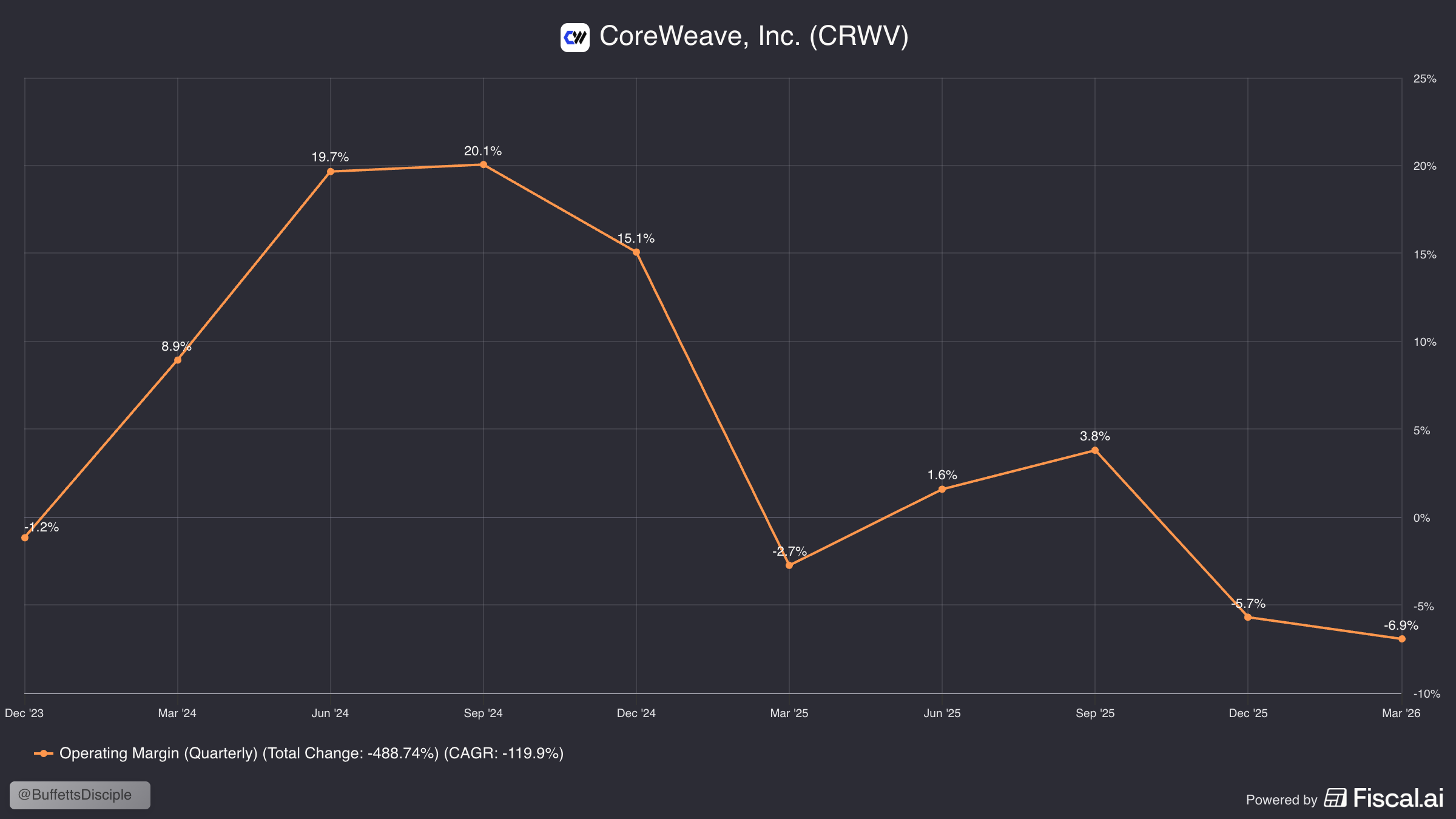

The recognition of this backlog is resulting in aggressive revenue growth. The current guidance is to deliver over $12B in revenue this year, a 100% increase over the prior year. This ramp, however, has been hurting their margins.

CoreWeave is essentially at its worst margins, maxed out on debt, and facing significant AI uncertainty. This is the cause of the stock's overhang. As the year progresses, these margins will expand, especially towards Q3. Anthropic and OpenAI’s ARR ramp will continue to grow aggressively, pushing the AI re-rate higher. As more clarity comes into the market, it should settle the fears on CoreWeave and give it a nice re-rate. One area in particular where I believe investors' fears will be eased is debt.

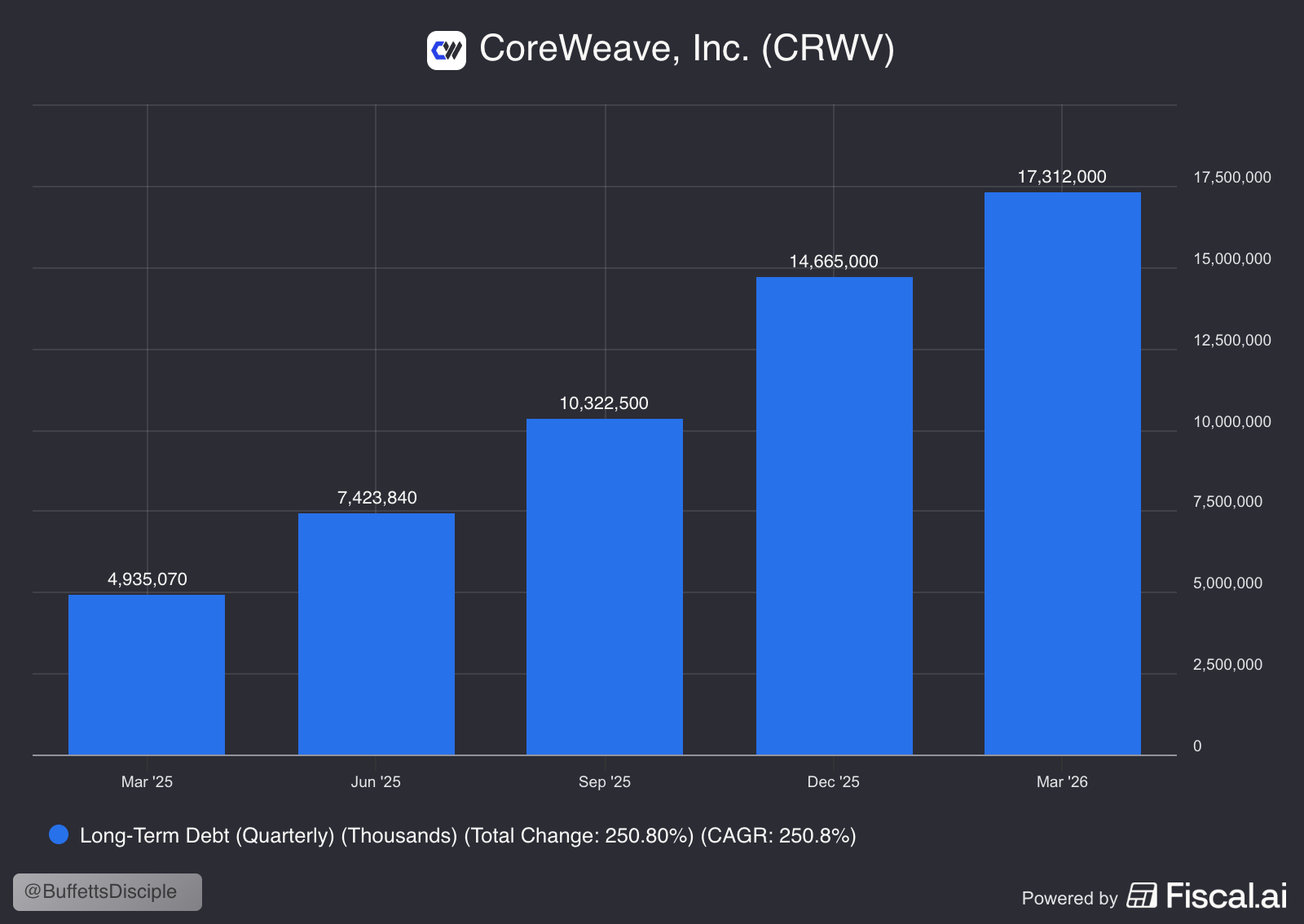

CoreWeave’s Debt

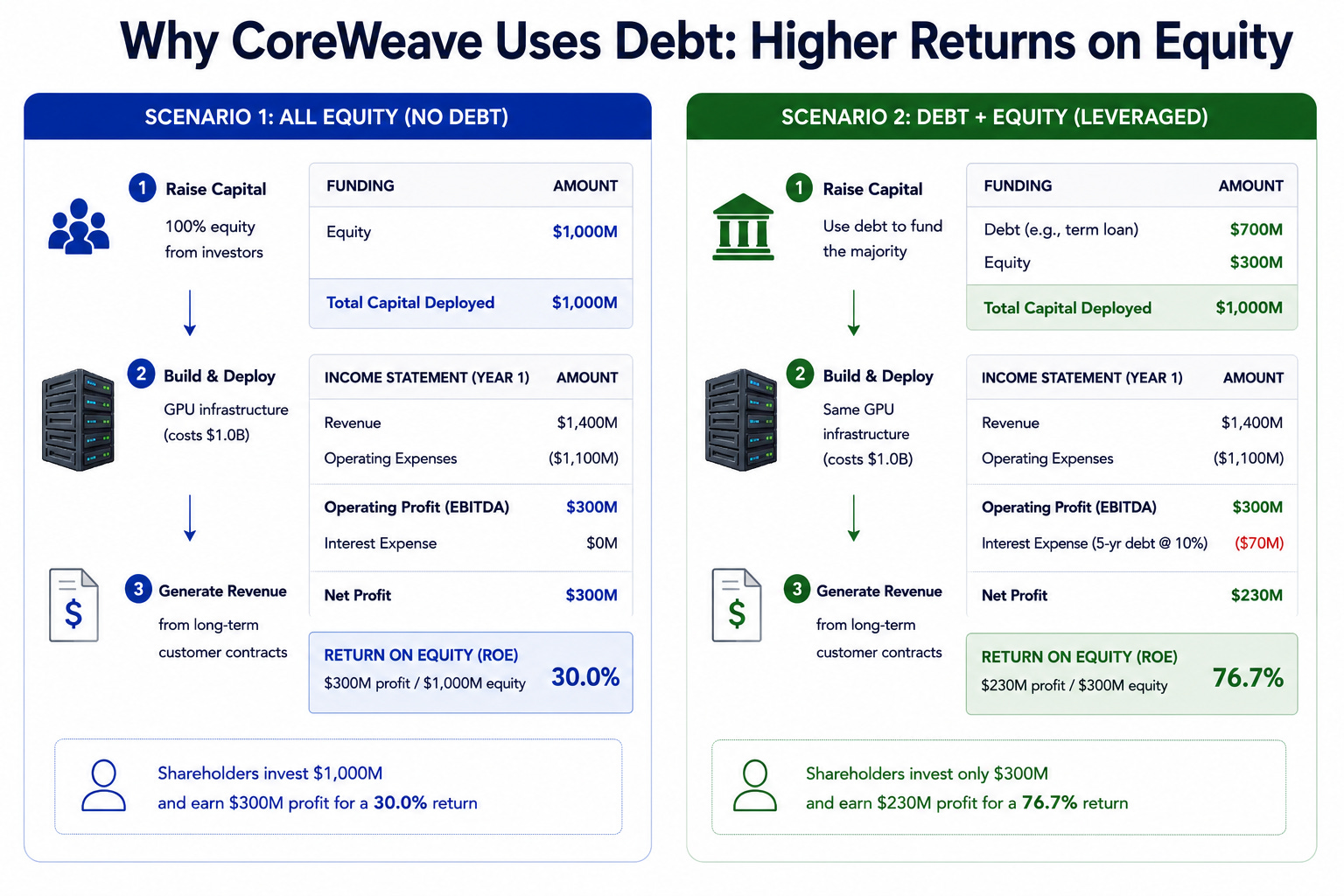

Over the last year, CoreWeave’s debt has gone from $5 billion to $17 billion. This rapid growth in debt has made investors uneasy; however, in my view, it is fundamentally the most misunderstood part of the entire business. Typically, when it comes to significant capex, businesses have several options. 1. They can use existing cash flows (which CoreWeave has little of) 2. They can dilute and raise money via the public markets, which CoreWeave has done some of. 3. They can utilize debt, reducing dilution and greatly expanding the number of contracts that can be fulfilled (CoreWeave’s preference). CoreWeave’s preference for debt over other options is well-founded, especially compared to dilution. Using debt reduces the amount of equity required to fulfill a contract, which significantly boosts ROE per datacenter deployed. The graphic below illustrates the difference between using 100% equity and an equity-versus-debt split.

CoreWeave’s return on equity is significantly higher because they use debt. In simpler terms, it allows the business to build more data centers using less of its own capital. Imagine CoreWeave wanted to commit only one billion of its own capital. They could either choose option A and fulfill one contract for a net profit of $300 million, or option B, in which they can fulfill three times as many contracts for approximately $690 million in profit. CoreWeave’s use of debt is to allow the business to grow as much and as fast as humanly possible. If that wasn’t enough, CoreWeave’s debt is fundamentally differentiated from most debt companies take on.

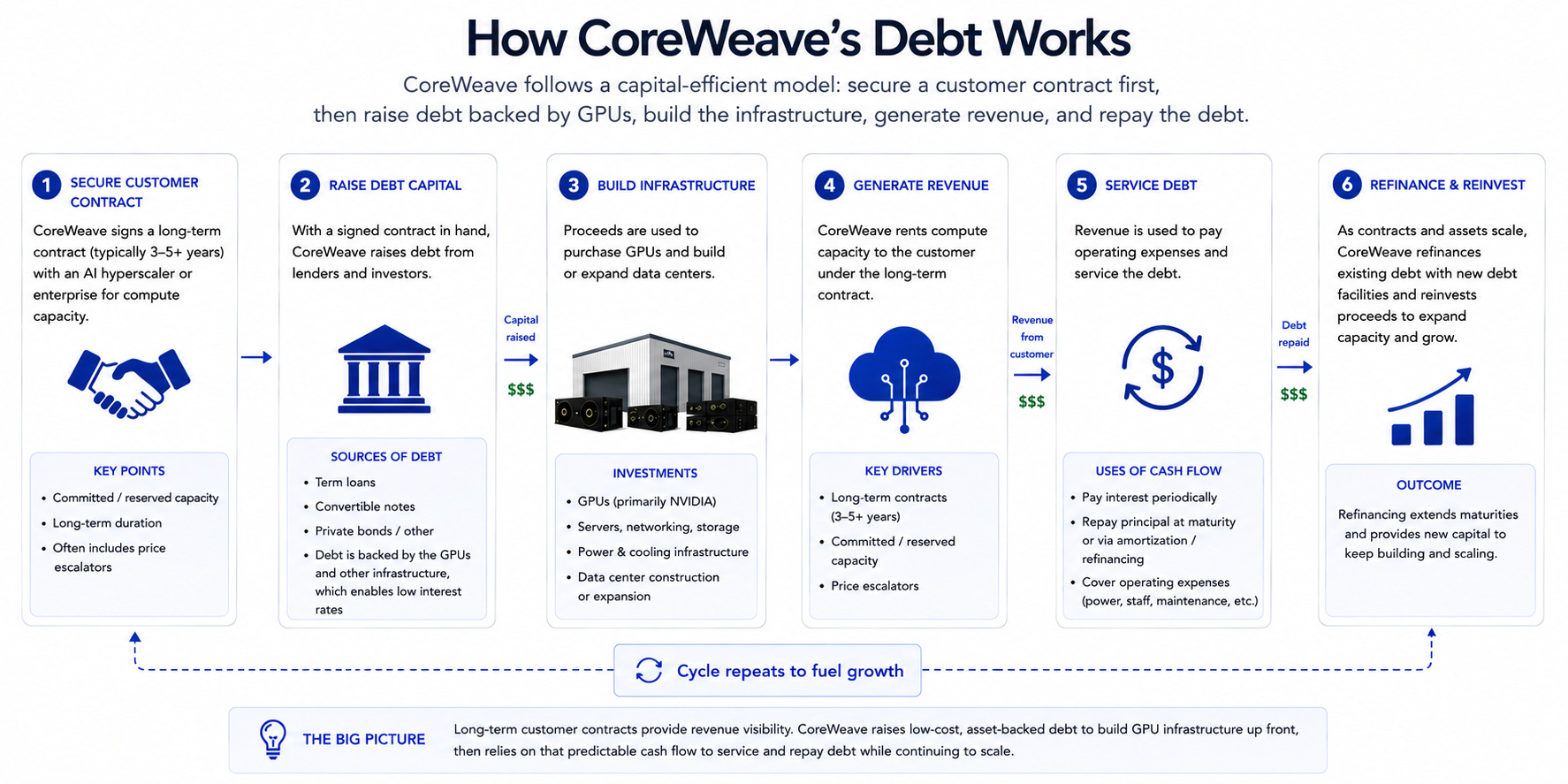

Most debt is speculative. It’s taken on for the acquisition of assets, believing they’ll return good money and improve the business’s future prospects. CoreWeave’s debt is solely to fulfill contracts, eliminating any speculation about future cash flows. The following diagram illustrates how it works

CoreWeave doesn’t raise debt until it secures a customer contract. This means the debt will be covered by the contract’s cash flow. So if CoreWeave takes on a billion dollars of debt, it’s only to service a contract worth more than a billion dollars. Which raises the reasonable question: if the contracts are profitable, how do we know the customers will honor them? This is a reasonable question, which I address in more detail later. In the meantime, just know that less than 30% of the backlog is AI labs (companies that are not profitable); the rest is with highly cash-flow-generative businesses.

The original cloud providers had core businesses before they started their cloud services, and they were able to use the cash flow from those businesses. Eventually, as CoreWeave scales, it will likely rely more on its own cash flows and less on debt. As things stand, though, they really only have two options, and as an investor, I’d much rather they minimize dilution and lean into cheap debt. Which leads me to the next major concern: is selling compute ultimately a commodity?

Are Neoclouds a commodity?

There are two parts to this answer: the business today and the business in the future. Starting with today, I’d say the business is “commodity-like.” A true commodity has no differentiation. Take gasoline. All you want is the lowest price. A business that is commodity-like has a level of differentiation. For example, banks are commodity-like, but they do have some pricing power and differentiation. As things stand, CoreWeave differentiates itself in the service it offers. It’s also why they’re able to charge a premium relative to some of their competitiors.

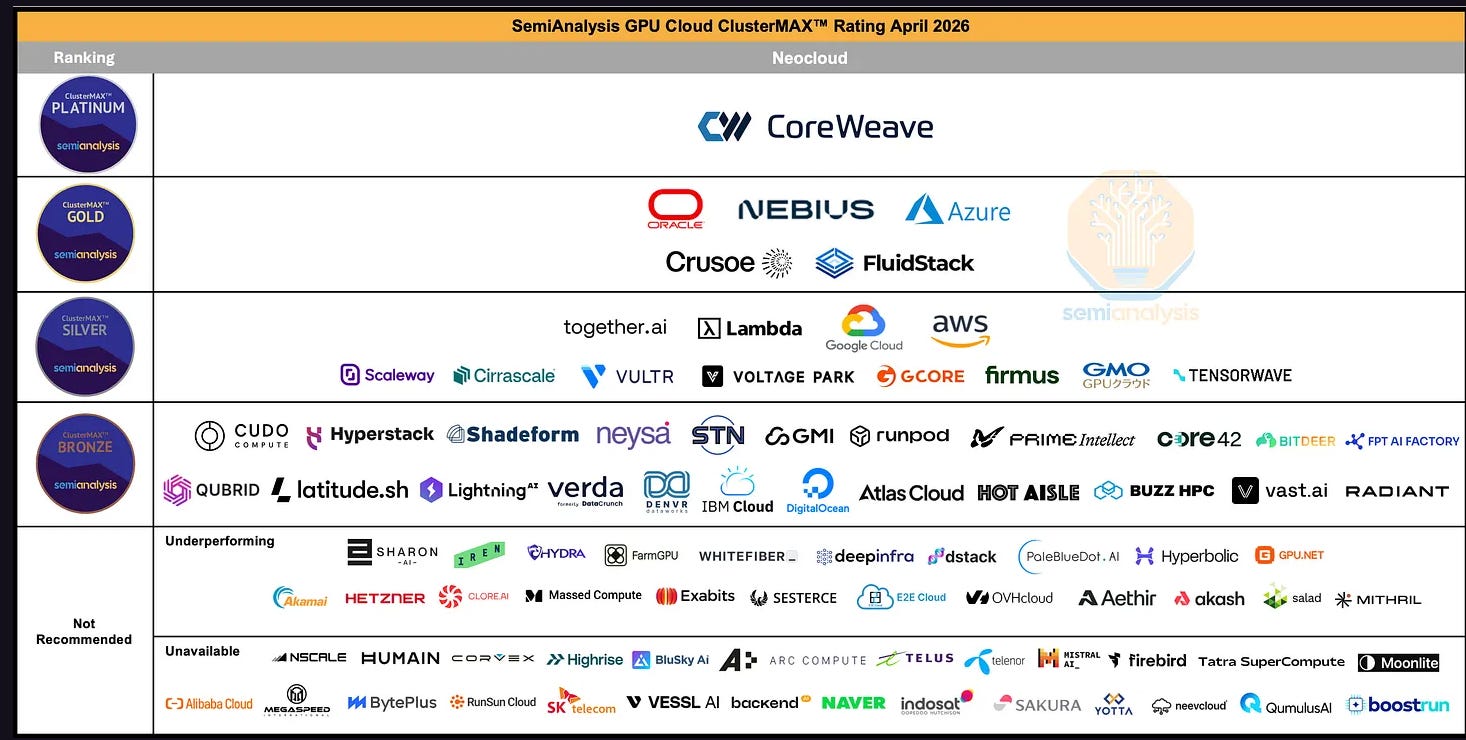

CoreWeave provides the best-in-class service for deploying, running, and maintaining NVIDIA GPU Clouds. This is best supported by the Semianalysis Cluster Max rating, which is based on 10 separate benchmarks: Security, Lifecycle, Orchestration, Storage, Networking, Reliability, Monitoring, Pricing, Partnerships, and Availability. CoreWeave is the only business to achieve the platinum rating twice. Beating out notable competitors such as Microsoft, Amazon, and Google. Something I’ve written about many times in my articles is the power of focus. It’s no coincidence that CoreWeave provides a better AI cloud service than everyone else, because it’s all they do.

The next generation of GPUs will be a step above where we are today in terms of complexity. Most companies will not take the risk of spending hundreds of millions or billions of dollars only to have their GPUs deployed incorrectly, with minimal utilization and poor customer service. As things stand, I believe that for many businesses, speed is the moat, and the premium to ensure your cloud is running properly is well worth it. CoreWeave superiority is further supported by their customer list.

For me, one of the most significant validations of the thesis was the recent contract with Anthropic. Anthropic has historically shunned NVIDIA GPUs, preferring Amazon’s Tranium or Google’s TPUs. There’s a bit of history as to why this is, and it goes beyond the scope of this article. Essentially, Anthropic and NVIDIA are at odds over past disagreements. However, NVIDIA GPUs offer significant flexibility and are quite powerful for exploring different directions in AI research. Anthropic is a leading AI lab. Everyone wants their business because it’s clear they’ll be a large customer. Choosing CoreWeave over everyone else is a major validation of the service that CoreWeave provides.

If customers’ sole focus were price and this were a true commodity, they’d be working with a no-name business that was willing to take no margin to validate their company, but obviously that’s not the case. Reliability, security, and customizability matter to these businesses. As things stand, in my opinion, CoreWeave will continue to have an edge in the foreseeable future, as customers will pay a premium to ensure the quality of their AI clouds.

I mentioned earlier that 70% of their business was not from AI labs. Companies like Microsoft, Meta, and IBM are on the customer list. These businesses are renting from CoreWeave, either for their own internal workforce or to sell the compute on to their own customers. In aggregate, these businesses generate hundreds of billions of dollars in free cash flow annually. This significantly reduces the risks of these contracts not being fulfilled.

It’s possible that, over a longer time horizon, CoreWeave will evolve beyond just a bare-metal compute product. If they start offering unique services or customer deployment configurations separate from their core offerings, it could become difficult to switch to other cloud providers. It would meaningfully change the economics and valuation of their business. Whether or not this ultimately happens, I don’t know; it’s hard to predict. I also don’t think it’s important for the thesis here, though. The business is cheap enough today. Simply staying the course will earn them the re-rate they deserve. If this part plays out, the re-rate will be higher.

Risks

NVIDIA

CoreWeave’s entire business is deploying NVIDIA GPUs. This concentration is a risk and should be acknowledged. If they cannot deploy these GPUs, they have no business. If, for any reason, NVIDIA decided not to sell to CoreWeave and could not fulfill its contracts, it would obviously be devastating to the company. I think the chances of this happening are near zero.

The other core risk is that NVIDIA stopped being the leading provider of GPUs. Either their product becomes commoditized, or a competitor provides higher-quality GPUs. In that case, you’d have fewer people turning to CoreWeave, since CoreWeave’s sole focus is NVIDIA GPUs. I think this is an extremely unlikely scenario in the foreseeable future, but it could become an issue someday.

Execution Risk

As great as a $100 billion backlog is, they still have to deliver data centers to realize it. They need to secure land, power, and chips, as well as labor, to deliver all these data centers. There are significant supply shortages in all of these, and the team will have to work quickly to secure everything they need to deploy these data centers on time. I personally believe if we’re talking about a risk relative to probability, this is the number one risk. It would especially hurt the stock in the short term if they start to fall behind. For what it’s worth, I don’t view this as a CoreWeave-specific issue but a broader industry supply issue. Data centers are also increasingly entering the public mind, and more regulation is expected in response. Supply shortages will eventually be worked through, but regulation could materially diminish the ability to put up data centers.

Debt/AI Bubble/Compute Glut

CoreWeave was built on navigating an extremely cyclical crypto mining market. During downturns, they would aggressively expand. I’d expect them to run the same playbook if we had a compute glut. It’s important to remember that the customer base is extremely diverse, with most of its customers being profitable, cash-flow-generating businesses. As long as they can survive a glut, they’d likely come out stronger. This would obviously hurt the stock price in the short term, but long term it could act as a tailwind. I believe a short-term glut is extremely unlikely, but it’s still worth acknowledging this risk.

Competition

This space is hyper-competitive. If CoreWeave does not provide a service on par with its competitors, it could fail to secure future contracts; it’s also possible, and even likely, that its competitors will continue to improve at deploying and servicing NVIDIA GPUs and eventually be on par with CoreWeave. Given that the only differentiation is their ability to deploy and run these servers, removing that edge would be detrimental. Given how quickly AI is advancing, it seems unlikely to me that this will happen soon.

Meta

Meta came into this year announcing record capex of $150B. Meta mentioned they could sell if they had excess capacity, but indicated they’d mostly use it for internal use cases. However, a week ago they publicly announced that they’d be looking to start selling this compute and becoming a cloud provider. This is generally seen as incredibly bearish for a company like CoreWeave, as it may indicate compute surplus and additional competition. I, however, do not see it this way.

Let me start with the obvious: if Meta’s goal is to enter this market, the most logical step would be to acquire CoreWeave. CoreWeave already has a massive backlog and is a massive operator in this space. They’d own the best operators while having cash flow to support the underlying business.

With that said, I do not think Meta is entering this market to directly compete with CoreWeave. CoreWeave is a high-quality, low-cost operator. The benefit is that you can secure a large volume of RPO; the downside is their margins. Overall business quality is not great. If Meta enters this segment of the market, it will materially reduce the overall quality of their business. I believe Meta’s objectives are much simpler, and that instead they’re looking to be more in line with Google/Amazon/SpaceX. The recent xAI deal is rumored to charge 2x the normal compute rate.

If that’s the case, I believe Meta will selectively rent compute when the rates justify it. This would maintain Meta’s overall business quality, increase revenue, and boost the share price. Ironically, I think if Meta competed directly with CoreWeave in a higher-volume, lower-margin business, it’d be a net negative for the share price, since overall business quality would decline significantly.

Google, AWS and Microsoft

The hyperscalers all deploy and run NVIDIA Cloud GPUs. Customers are generally willing to turn to a business like CoreWeave because it provides better service at a better price. Obviously, it’s possible that the hyperscalers eventually become on par in terms of service and even pricing. While this might seem likely, I’m less convinced. I always value companies that have focus, and CoreWeave has one singular focus. It’s also why they provide the best service. Hyperscalers are running dozens of businesses at the same time, and their clouds are much larger in size and complexity.

Good companies like Google, Microsoft, and Amazon already have benefits that many companies use their clouds and don’t want to switch to another cloud. So even though they provide a lower-quality service, many businesses are okay with that for the simplicity. Over a sufficiently long period, it seems inevitable that these companies will provide a service on par with CoreWeave’s. Given the current pace of change in AI, though, I believe this is years away.

Potential Concerns/Comments

Memory

Memory costs have exploded, which could be seen as a threat to CoreWeave. If they have fixed-price contracts and input costs go up, won’t that affect their margins? In the case of CoreWeave, no. Their contracts are structured to account for the underlying cost of materials when they know it; if they don’t, they leave it floating in case input costs go up.

Nebius

We cannot talk about CoreWeave without talking about Nebius. Nebius is another neo cloud and is often considered the better one by most retail investors, largely because of its founders and perhaps because it uses far less debt. I believe retail investors’ read on this has been correct, given that Nebius stock has far outperformed CoreWeave.

As things stand, though, I’d argue CoreWeave is cheaper, given its current fundamentals. I believe CoreWeave will see a similar re-rate to the one Nebius has seen recently. If I had to describe the main difference between Nebius and CoreWeave, my personal opinion is that Nebius is aiming to evolve beyond a bare-metal compute cloud and more like an “AWS of AI”. If they do so successfully, it’s likely to have a more long-term sustainable business.

I don’t actually think Nebius is CoreWeave’s main competition, even though they share similarities. Most of the demand and supply is being sucked up by the hyperscalers, not Nebius. If CoreWeave fails, it seems unlikely to me that Nebius would be the reason, and vice versa. I think investors can do well owning both names or picking one they prefer.

Opensource models

There are concerns about open-source models and the commoditization of the industry. A company like CoreWeave cares only about the amount of compute being consumed. Whether it’s on a proprietary model or an open-source model does not change that. The growth of open-source models will only make AI more readily available and cheaper, increasing consumption and demand for CoreWeave’s product offering.

Additionally, open-source models are often used as a starting point for developing proprietary or domain-specific models. This will only drive further demand for training, which will in turn increase demand for NVIDIA GPUs.

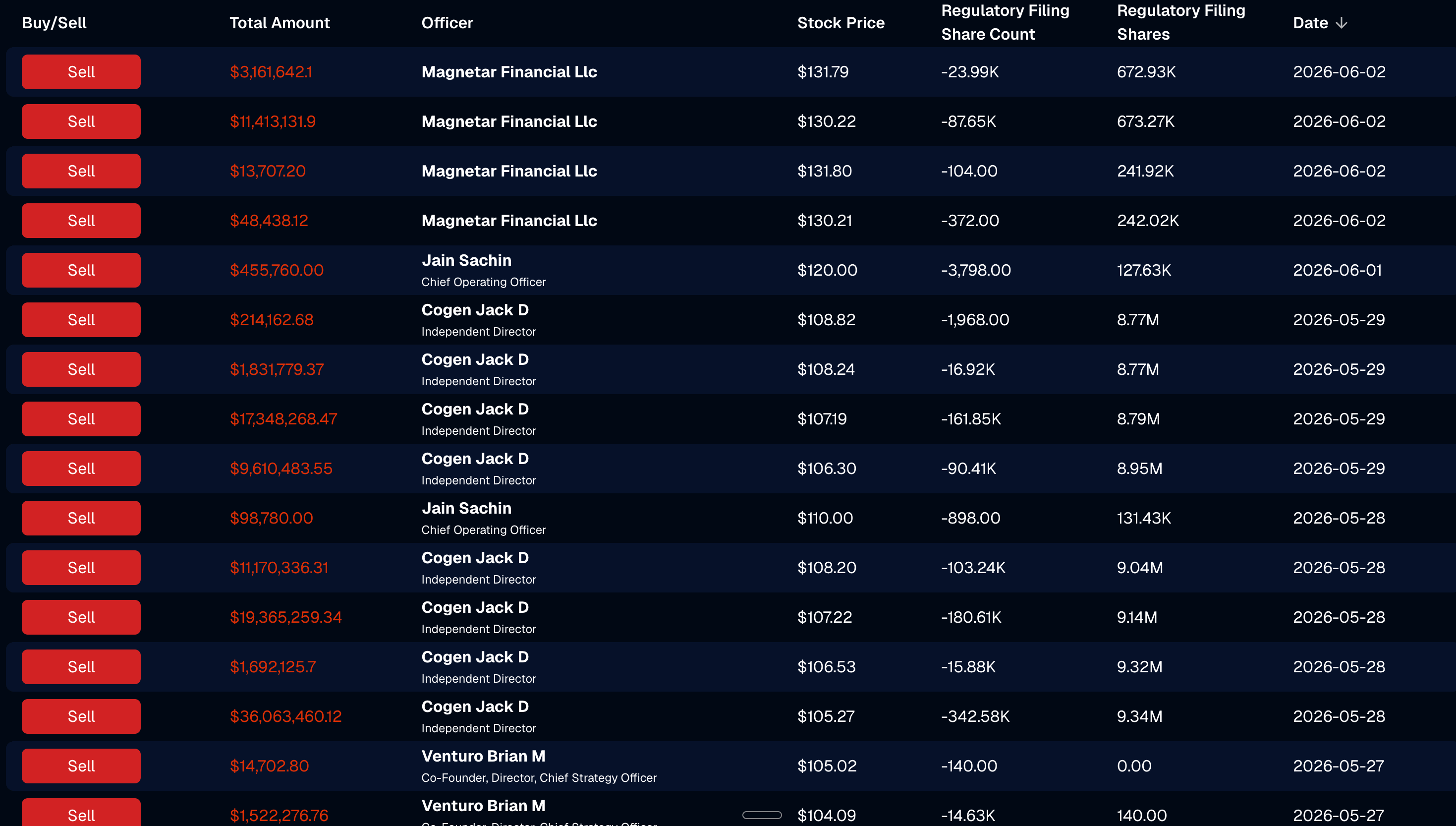

Insider Selling

I want to be clear. The level of insider selling at this company is not ideal and is a major drag on the share price. It’s pretty obvious to me that a number of folks are trying to exit their positions entirely and will continue to do so any time the stock exceeds the $100+ range. I believe the fundamentals will eventually outweigh this drag, and once a number of companies, especially Magnetar Financials, have fully exited, it should allow the business to re-rate. Otherwise, I personally do not take much meaning from insider selling.

Valuation

Nebius currently trades at the same market cap as CoreWeave, while guiding to less than half of CoreWeave's exit ARR this year. If we assume a 1-for-1 re-rating, CoreWeave will double. For what it’s worth, I don’t think CoreWeave deserves a one-for-one, but even if we assume Nebius should get a 50% premium, that would still imply roughly 30-40% upside for CoreWeave today. My personal price target of $115 is based on this price discrepancy. I think that it accurately accounts for the debt risk while giving CoreWeave a reasonable valuation relative to Nebius.

Conclusion

Folks, I want to be super clear. This is not a traditional value play that I make. Most of my investments trade on clear fundamentals, and as long as they keep delivering, they’ll often trade within 10x earnings in a few years. CoreWeave is not that type of play.

This is a bet on simply the underlying fundamentals of CoreWeave coming to fruition: the business expanding margins, delivering profitability, and investors coming to understand exactly how their business works. I believe this will become especially true over the next couple of years, as they start to work through the majority of their backlog and can use more of their cash flows and less debt to expand their business.

This is also just a bet on the broader AI tailwind that will be at the back of the market over the next few years. Investors are constantly jittery about the amount of capex being spent on AI. However, I think there’s a very strong argument that this investment will pay out. Mostly, I trust the CEOs of the world's biggest companies to do basic math. As fears around the AI trade subside, I expect some of the more volatile names to re-rate higher.